150k American Express Business Platinum Offer

Update: The code no longer seems to be working when calling in. This deal is no longer active.

I had heard rumblings of a 150,000 point offer on the American Express Business Platinum card, but the offer information remained private. Then last night Doctor of Credit decided to share it publicly. I wrote about it briefly as a Quick Deal, but I thought that it warranted a more detailed look here.

The Offer

Receive 150,000 Membership Rewards points after spending $20,000 during the first 3 months. The $450 annual fee is NOT WAIVED the first year. This offer can only be applied for via the telephone and it expires tomorrow 5/15/2015.

To apply:

- Call 1-877-628-6736

- Provide them with this offer code: L081-994-816-5743

First Year Value

So lets look at the value of this offer. There is some debate as to the value of Membership Rewards points. Frequent Miler lists them as worth $.01 each on his Fair Trading Prices, while Ben at One Mile at a Time says they are worth 1.8 cents each. Given the transfer bonuses and other factors, a conservative value for me is 1.5 cents each.

If we use a 1.5 cent valuation, the sign-up bonus is worth 2,250. Subtract out the annual fee and you come out $1,800 ahead! There are also other benefits that may add to your value.

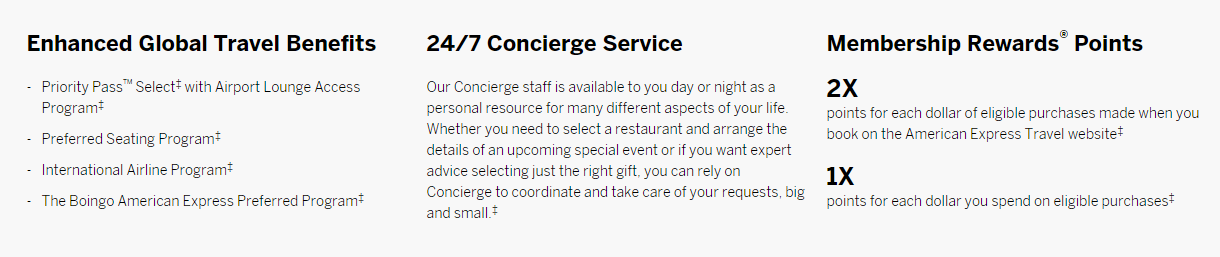

- $200 airfare credit per calendar year. (You would be able to get one in 2015 & one in 2016.)

- $100 Global Entry credit

- SPG Gold Status

- Priority Pass, Delta and Amex Centurion Lounge Access

- Other small benefits such as Boingo, etc.

You can find out all of the benefits and more info about the card here.

Factoring in all of the ancillary benefits, this bonus is easily worth $2,000. But of course there is a huge $20k catch. (See below.)

Things to Consider Before Applying

- This is a business card, so do need some sort of a business to apply. With that said, you don’t need an Employer Identification Number. Your social security number will work fine and American Express will judge your application based on a number of factors including credit, personal income and business income.

- You have to spend $20k in the first three months. That is a huge amount for a lot of people. There are many ways to meet this requirement, but the easiest would probably be to buy $500 gift cards for $3.95 each at a mall. When doing this, you would need to purchase 40 cards for a cost of $158. In the end though you would have 170,000 total points. (Another way to think of it is your $158 cost of MS generates $300 in points.)

The $20k Spending Challenge

A couple of bloggers decided to use this deal to start a contest called the $20k Platinum Spending Challenge. These bloggers (and a few readers) will be doing their best to make a profit while hitting the $20k limit. Some of them will be gift card churning while others will be reselling. You can find out more info over at Money Metagame.

Conclusion

This really is a fantastic offer if you can manage the spending requirement. If not, Doctor of Credit has a list of lesser Platinum card offers including a 100k point offer with a $10k spending requirement. Whether or not you get the Business Platinum, it should be fun to follow along and learn a few things about MSing through reselling and churning gift cards! Do you plan on applying? Let me know in the comments.

Lower Spend - Chase Ink Business Preferred® 100K!

Chase Ink Business Preferred® is a powerful card that earns 3X Ultimate Rewards points in a broad range of business categories on the first $150K in spend per year. Right now earn 100K Chase Ultimate Rewards points after

Chase Ink Business Preferred® is a powerful card that earns 3X Ultimate Rewards points in a broad range of business categories on the first $150K in spend per year. Right now earn 100K Chase Ultimate Rewards points after Learn more about this card and its features!

Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.

{kind=link}

Shame on me for not performing more thorough customer sentiment research before signing my team up for our American Express Business Platinum cards.

I run an eCommerce startup in the apparel space and like many, was dazzled by the prestige and membership “benefits” that American Express is supposedly known for. I applied for this card, which was a much easier process than I anticipated (a facade…keep reading). I was approved almost instantly and signed my CFO up for a Platinum Business card as well.

We made it through 2 weeks of card use before the issues started rolling in.

I am not naive enough to believe an unlimited monthly spending limit is truly possible. What I do expect is for my spending projections, annual revenue and personal income to be considered intelligently by a rational human being and not solely by a computer algorithm that is clearly flawed. Despite indicating a minimum monthly requirement of $10,000 (a pretty modest limit, all things considered) we were assigned a $6000 limit. Unknowingly, I might add. It wasn’t until my CFO was mid-travel that we discovered this to be the case.

After a hour on the phone I was informed that we needed to “prove a track record” of spending and payment before they could increase the limit. I paid the entire balance instantly. The card was up and running again once the payment posted (remember, we’re 2 weeks in here). Total monthly spend and payment month 1: $16000. Multiple payments were made in the first month, all before they were even close to being due.

This behavior repeated during month 2 as well. We had the same issues with the card being shut off for spending that we advised them of in advance during the application process and the same behavior of making multiple payments early to try to “prove our track record” as they say.

Furthermore, when you ask their customer service representatives how the calculation for credit limit increase is performed they will not be able to tell you. I asked what we could expect our increase to be for the next month if our spending/payment behavior was as they suggested and was told that there wasn’t any real way of telling. You are American Express! You don’t know how your algorithms work?!

Month 3 rolled around and we were at our wits-end. The second week of month 3 I was in the middle of business travel and took out my card to pay for something. Declined. This was not only impressively inconvenient, it was also mortifying. We paid all of our bills early and made multiple payments per month. This was the last straw.

I called American Express Business Platinum “customer service” to find out what the issue was now. News to me, they do a “financial review” on month 3. Now the easy application process made sense. They were requesting 2 years of income statements, tax returns…everything I expected they would have handled upfront.

This is the shadiest customer acquisition process I have had the displeasure of being unknowingly subjected to. Whatever was required for card approval should have been handled at the genesis of the engagement. Period.

Mind you, I am in another state traveling for work. This came without any warning. I pleaded with customer service to turn the card on until I could return home from business to gather the requested documents. They said this could not be done. That was it. I cancelled the card on the spot. I was never confident that when I took the card out it would actually work. I could not keep running my business with a card so unreliable.

But wait, there’s more!

Over the course of the very brief time we had the cards we accrued close to 90,000 points. Imagine my surprise when I logged into my account a few days later to find they were gone.

To make an already long story a bit shorter, American Express is not required to disclose to you when you are cancelling your card that they will wipe the points from your account immediately upon account closure. Why, you might ask.

Several phone calls and multiple hours of my time speaking with the American Express Business Platinum “customer service” team led me to the following discovery.

Do you remember that brick of a contract that they packaged so beautifully with your American Express Business Platinum card when you first got it? READ IT CAREFULLY. Memorize it. That discloses every shady thing that American Express will be doing to you over the course of your time as their client. Because it is stated in there, they were not required to advise me of the point seizure upon account closure.

This is easily the worst tool any startup could get locked into. American Express should be ashamed of the way they treat small business owners. We were impeccable customers to them. I will NEVER give my business to them or anything they stand to benefit from ever again. Nor will anyone who asks about my opinion of American Express, I can assure you.

[…] year I wrote about and completed a 150K bonus on the American Express Business Platinum card. That offer gave 100K Membership Rewards points after $10K in spend during the first 3 months and […]

[…] before flights. Their Amex Offers programs has also been very generous and who can argue with that 150K bonus on the Business Platinum last year? On the flip side though is my realization over time that they simply aren’t the […]

[…] would wait for a better offer. We have seen a number of 100K offers surface and we even had that monster 150K offer earlier this year. For only 75K Membership Rewards (with a very high spend requirement) I would […]

You losers killed this. Could’ve lived indefinitely if not for a couple of wise ass bloggers that stole this from the person that was kind enough to give this out to people, on condition that they not post it online. What jackasses. I’m sure people that read your blog think that you’re clever and a great asset to the game, but they don’t realize how much better it would be of you would stay far away from this. Please don’t steal, be ethical, don’t be stupid, and shut this stupid copy and paste blog. Thank you kindly.

[…] Any time a bank wants me to pay a $450 annual fee I am skeptical. Of course this year’s crazy bonus offers have enticed me to sign-up, but it will be long term benefits that will ultimately convince me to […]

I think it is now dead. Others also report code no longer working.

The code worked for me at 3pm Eastern time.

It’s not the only RSVP code out there. I was targeted for the 150K offer and it’s much different

Yes the code mentioned here is dead, however I’m sure other people were targeted with their own code.

The way this works is that the code only works online one time, but it works many times when calling in.

Ouch, waited until I got home from work to call in for this one. Got the code from MilesPerDay a couple weeks ago but completely forgot about it as I went away to Ireland and France for two weeks (just got back last night). Hope someone else posts another 150k RSVP code that we can use to call in with soon…would have been a great deal to get in on.

Just tried calling, the rep told me that offer code “was no longer available” and offered me 25k for the Biz Rew Gold… didn’t even ask how much my company made.

Does this happen and people call back, or have others found it no longer out there?

Thanks so much for the heads up! I saw this after my morning app-o-rama (applied for 6 cards), so I thought I would be turned down for too many recent applications. But the rep was very nice and I was approved immediately! Woo hoo!

Are we certain we can MS via GCM VGC purchases? I just applied and rep mentioned purchases of cash equivalents would not be qualified purchased. But I believe those GCM transactions go through Amex as a retail purchase.

That is standard language, but these purchases have always counted. You could always make a small purchase and then verify that it counts.

And a great way to get targeted for an Amex FR, which trust me, is not pretty

A financial review is typically only an issue if you lie about your income on a tax return. With that said, everyone needs to make their own decision and there are always risks.

Thanks for bringing the FR up, because that is always a risk for people.

[…] MilesToMemories: Huge 150k Sign-Up Bonus for Amex Business Platinum & the $20k Platinum Spending Challenge […]

This is a great offer. I really appreciate you posting it.

Would using this card to load Serve count toward minimum spend? If so, could AUs load another $1k-1.5k per month to their own Serve accounts?

Also, per DoC (http://www.doctorofcredit.com/does-funding-a-bank-account-with-a-credit-card-count-as-a-purchase-or-cash-advance/) it seems you can use an AmEx card to fund the opening deposit of up to $500 on a new U.S. Bank checking and another $500 on a new savings account without incurring cash advance fees. I don’t see why you couldn’t open more than one checking and savings account.

People have reported that using Serve online loads works towards minimum spend, although you don’t get rewards. I can’t confirm this personally, but I have heard it from a few people. As for the bank option, that seems way too complicated.

I still fail to see the value of the Amex Plat in this day and age–even with the 150k bonus. You have to spend a guaranteed $450 to get the card, and you may not hit the $20k spend. Even if you do, the card has no bonus point categories for future spending, and you’re still stuck with that huge annual fee. We’ve already got Global Entry. I’m already SPG Plat. LAX/SNA from where I fly doesn’t have a Centurion lounge. (Only SFO has one where I fly regularly.) I almost never fly DL, so the lounge benefit there is worthless. FHR benefit is now easily matched by using a Virtuoso travel agent, so that’s not worth it. The $200 airline rebate would be nice–to make the annual fee only $250, still a lot. CSP has better rental car insurance (primary). While getting 150k MR bonus points would be nice, the loss of bonus points for that $20k spend with my SPG Business Amex or Chase Ink Plus/Bold or even my Amex BRG means that I could have earned equivalent points value with a card I already have–for no annual fee. (And my Amex BRG retention bonus gave me 30k MR points and $100 credit off annual fee.) So the Amex Plat is just not worth it these days IMO unless you really need MR points badly. Until Amex Plat starts giving bonus categories to justify its annual fee, it will rarely be worth it.

Gogo passes aren’t bad. I use the priority passes, and fly out of sfo frequently. Realize you can get the $200 twice and pay for global entry for someone else.

Nice one. If I have the Amex Business Gold, am I ineligible for this bonus?

No you wouldn’t be ineligible. The only way to be ineligible is if you have had the Business Platinum in the past 12 months.

This same card also has the 100K points bonus on $10K of spend. So, if you get the card and don’t make it to $20K, you will still get 100K points.

An amazing offer, and thanks for getting the word out. My quandary is that I did a round of applications about 7 weeks ago, including a personal Amex. Do you have any knowledge or experience regarding another application less than 90 days after the last one?

They don’t have a hard limit like some other providers. Of course the approval will be based on a number of factors, but you shouldn’t have an issue based on having applied for a different card 7 weeks ago, especially since it was for a personal Amex. I have actually been approved for both a personal and a business card on the same day before.